[ad_1]

The Wall Street Journal reports that banks will recast mortgage loans. Thanks to Federal Reserve policy changes, it’s currently cheaper for banks to get loans than it has been for a while. The other effect of a reduced LIBOR rate seems to be lower mortgage rates. Rates have been declining for decades. Depending on when you opened a new mortgage in 2018, it would have been among the lowest rates historically available.

More Disposable Income = Growing Economy/Retail Investment

While there isn’t a direct correlation between mortgage rates and the overall stock market, the fixed cost of mortgages is money that is immediately not available to invest or spend. Lower rates, especially for the best-qualified buyers, can, therefore, equate to increased capital available for investment.

Mortgage-backed securities perform not just on the success of the loans, but also on the sale of new mortgages. Lower rates clearly equate to increased sales. All these factors can contribute to a more bullish market situation. MBG replicates “as closely as possible, the price and yield performance of the Barclays Capital U.S. MBS Index (the Index). The Index measures the performance of the United States Agency mortgage pass-through segment of the United States investment grade bond market.”

{kind=link}

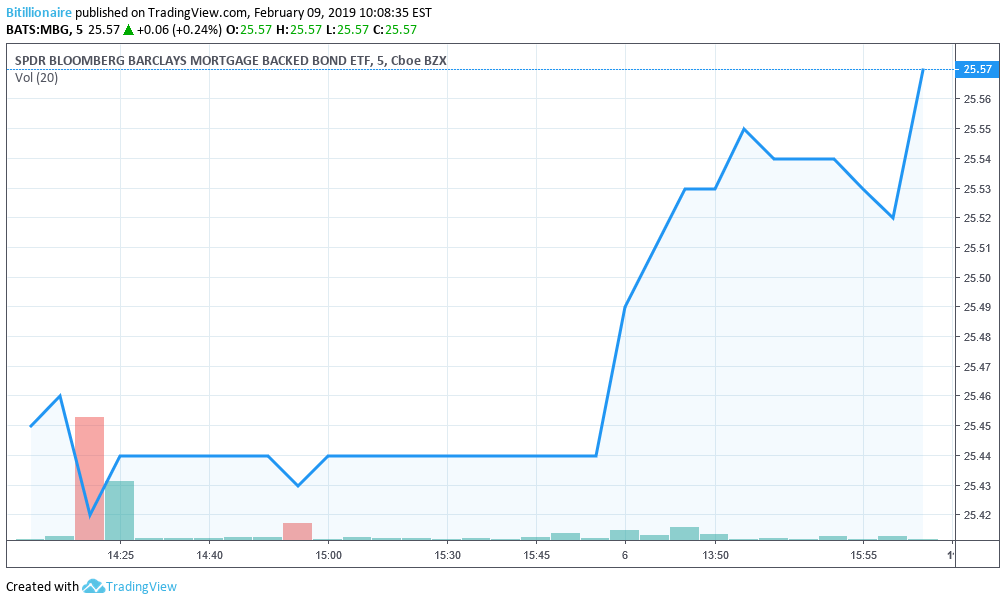

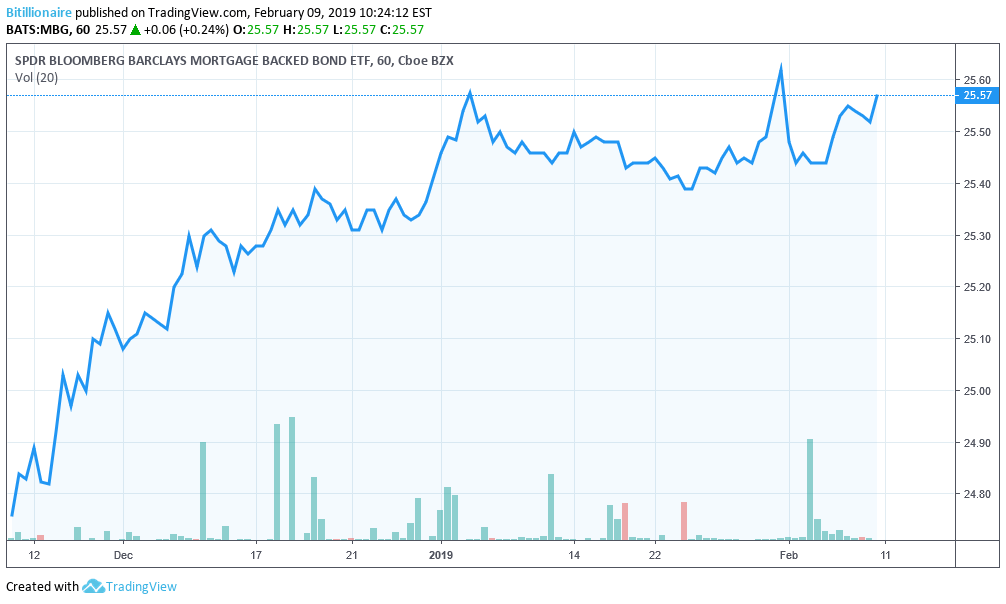

MBG is currently working toward surpassing its three-month high of $25.61. Friday’s trading pushed it all the way to $25.57. Volume was heavier near the beginning of the week. MBG is one of several good indicators to survey the health of the mortgage market. Here’s that 3-month chart:

The 3-month high was just a few cents higher than the close on Friday for MBG.

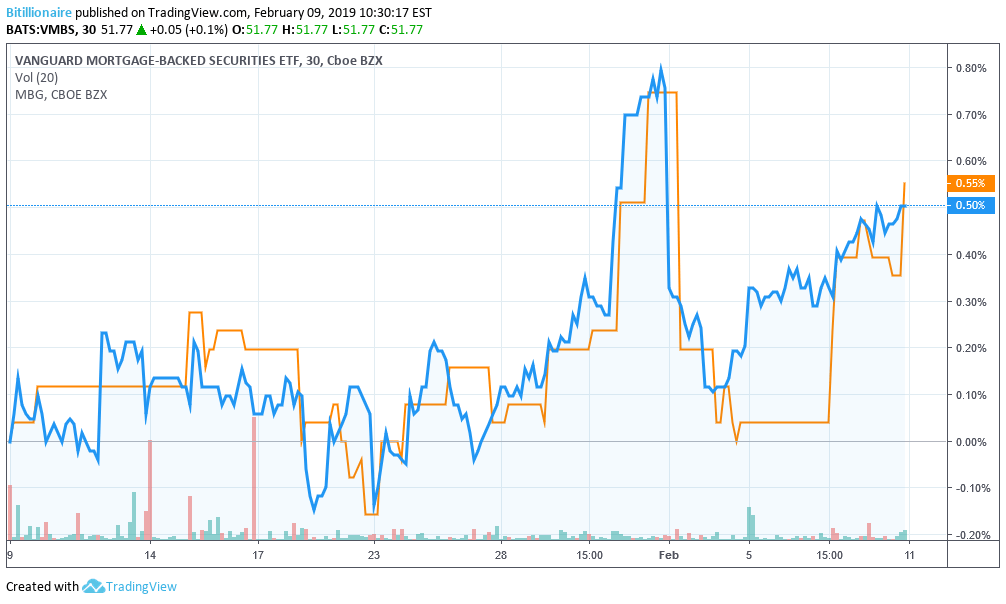

MBG isn’t the only one that’s been building momentum. The Vanguard Mortgage-Backed Securities ETF has been growing at about the same pace.

While we’re far from the housing bubble that contributed to the global financial crisis, it certainly seems the market is bullish on mortgages and bonds related to them.

The progress of MBG is tracked closely by VMBS, an ETF based on mortgage-backed securities.

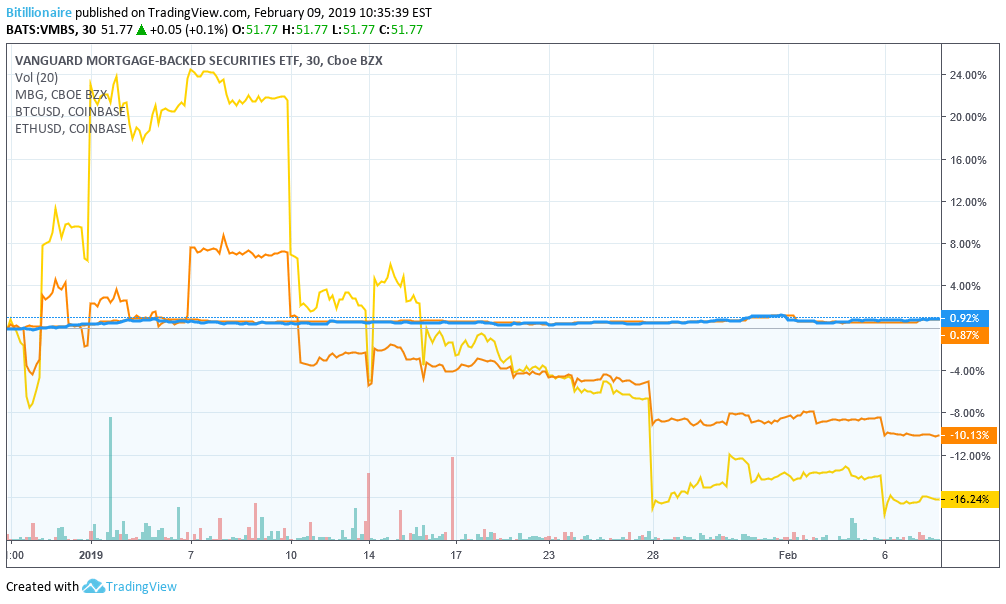

The Crypto Market Versus Mortgage Securities

There’s another aspect of lower mortgage rates to explore, however. On a macro level, they also increase the money available to invest in cryptocurrencies. Now let’s add to this chart the performance of Ethereum and Bitcoin over the same period, just to see what happens.

MBG and VMBS would have been a safer haven for money than major Bitcoin and other major crypto assets in recent times.

Ethereum and Bitcoin have both lost, while the mortgage markets have sustained small but steady gains. Short-term charts of these mortgage symbols show some chaos. But investing the exact same sums in mortgages would have earned you a palpable return in the interim, as neither ETH nor BTC has yet made a full recovery to December levels.

Reading too deeply into this chart might give one the impression that people were selling their cryptos and buying mortgages. That’s likely an exotic case study.

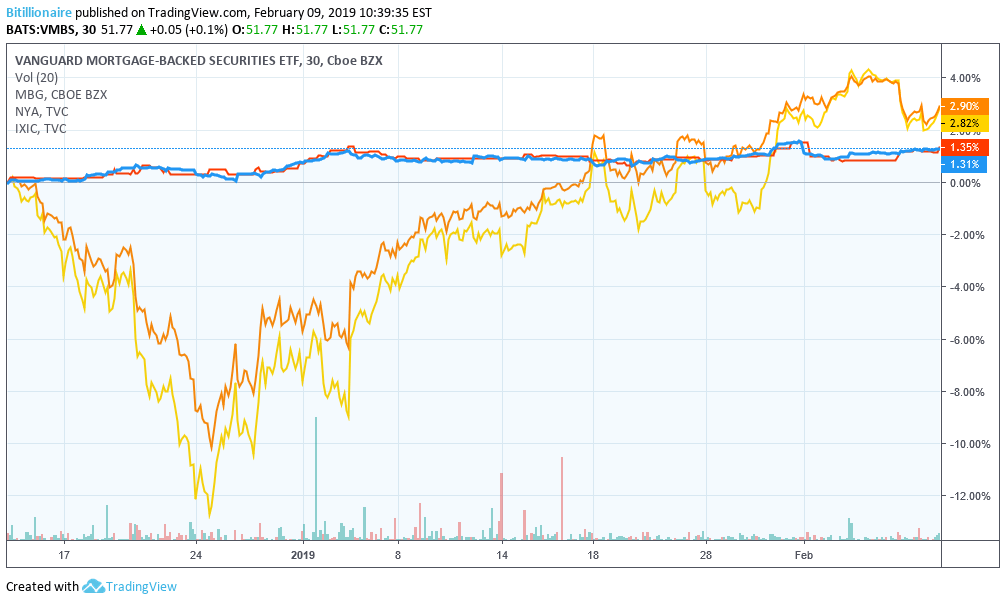

Now, how do the broader markets chart against these mortgage securities?

Notice that when the stock market dipped, mortgages held strong.

What we see here is that when the broader markets do poorly, mortgage security performance is largely unaffected. This is because these securities are driven more by government policy and loan performance, which by and large aren’t dependent on the performance of the stock market.

Lower Mortgage Rates Mean Stronger Markets

Yet, when the stock markets begin to chart higher, or vice versa, so too do the mortgage markets. The correlation there is about twice the percentage-wise gains: NYA and IXIC gain about 3 percent over the same period that MBG and VBMS gain roughly 1.5.

Lower mortgage rates are only a bad thing if you’re looking to pay your home off sooner. 15-year rates are consistently lower. It seems that, as the market goes, the more money banks have to loan out at a cheaper rate, the better the market can perform. Not only because real estate investors have excess capital to generate activity in other departments, but also because Americans then have more money in their pockets to spend in the now, in ways that generate favorable earnings calls — or speculate on the front end of the next great cryptocurrency bull run.

Featured Image from Shutterstock. Price Charts from TradingView.

[ad_2]

Source link