[ad_1]

By CCN: With all the hype about blockchains and their many uses, we shouldn’t forget the original purpose for the Bitcoin blockchain and Nakamoto’s great leap forward.

Blockchains and cryptocurrencies were created to be decentralized currencies, replacing or complementing fiat currencies. For the most avid crypto fans, crypto is the future of currency and will eventually handle full-scale economies. We dream of the day that we laugh and tell our kids and grandkids that we had physical wallets, paper currencies, and things called “credit cards” (“Grandpa, seriously, you are so old!”).

Preparing the Crypto Economy for Mass Adoption

So what has to happen in order for us to run economies on the blockchain?

There are several hurdles we still need to clear, like getting the value of these currencies to be stable, handling privacy in a sensible way, and getting confirmation speeds fast enough for point-of-sale transactions.

By far the most glaring hurdle, however, is throughput. We need to be able to handle many, many more transactions per second than any current blockchain is capable of. At 13 transactions per second (a high estimate), Bitcoin can handle just over a million transactions per day. For niche, small economies, this might do the trick. But it certainly won’t do it for, say, the US economy.

Let’s put this into perspective. In 2017, the US gross domestic product (GDP) was almost $20 trillion. GDP isn’t a great measure of how much money changes hands during the year, but for our purposes, it’s close enough. If about $20 trillion changed hands in the US in 2017, then about $54 billion changed hands every day (20 trillion divided by 365). Ignoring how slowly Bitcoin processes transactions, if it were to handle $54 billion in transactions in one day, transactions would have to be on average about $54,000 (54 billion divided by 1 million).

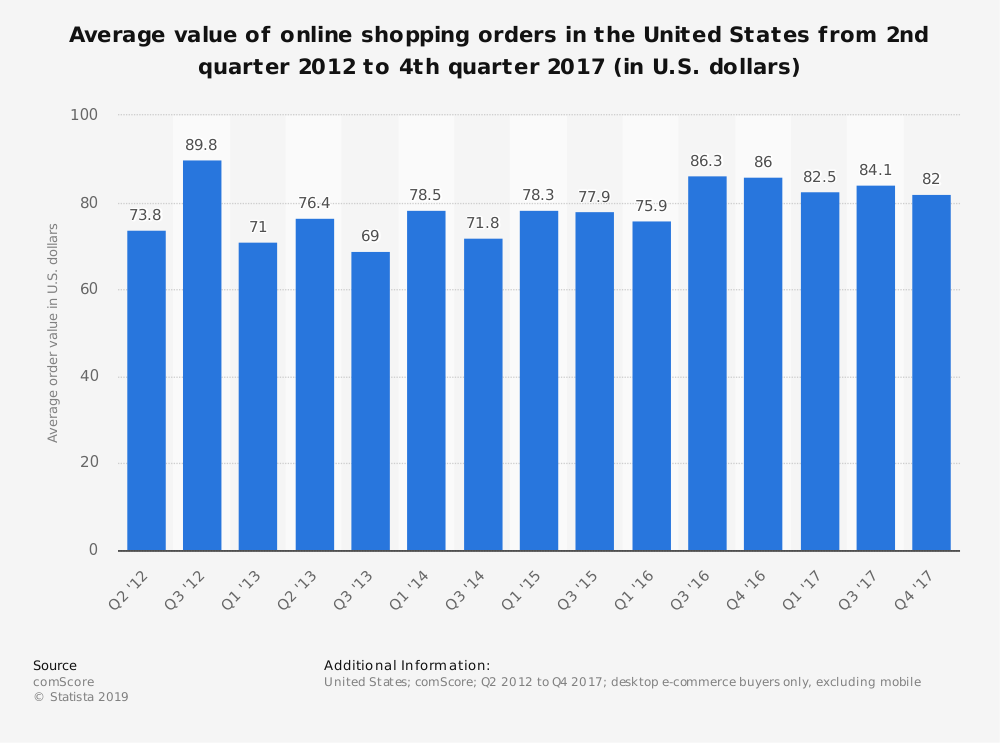

What? Your everyday transactions aren’t $54,000 on average? Of course not. Between 2012 and 2017, US consumers spent roughly $80 per transaction online.

{kind=link}

Bitcoin doesn’t look like a candidate to replace credit cards in the online payments realm. | Source: Statista

In 2016, transactions on Amex credit cards averaged about $141, and those on Visa averaged about $80. While it is true that corporations tend to transact in higher dollar amounts, it’s still likely that the crypto community is still a few orders of magnitude away from being able to handle all the transactions in an economy on a single blockchain.

If, based on the statistics I just gave, we assume that transactions are about $100 on average, then $54 billion would change hands every day in roughly 540 million transactions (54 billion divided by 100). That boils down to about 6,000 transactions per second on average. If we take into account the fact that most people transact during the day, a quick recalculation yields about 10,000 transactions in an average daytime second (instead of dividing by 24 hours of the day, divide by 16 to account for about 8 hours of sleep).

This estimate is probably about right. There are roughly 324 million people in the United States, and about 5 million businesses. If we assume that people and businesses, on average, transact 1.5 times per day, then we have about 500 million transactions per day (329 million entities multiplied by 1.5). This is close to our estimate of 540 million daily transactions from before, which gives about 10,000 transactions per daytime second in the United States.

Bitcoin Would Need to Increase Transaction Capacity By Four Orders of Magnitude to Replace Visa

With Bitcoin’s staggeringly-limited transaction capacity, it’s unrealistic to believe it can rival Visa or Mastercard – much less both. | Source: Shutterstock

Getting back to the original question, how many transactions per second does a blockchain have to be able to handle in order to support the United States economy? Our rough calculation of 10,000 transactions per second is almost certainly not enough, but it does give a base from which we can work. To give perspective, Visa processes about 1,700 transactions per second on average but at peak times it can handle up to about 24,000 transactions per second. Their max limit is just over an order of magnitude higher than the average, in order to handle high-volume days like Black Friday or the post-Christmas wave of returns.

Taking Visa’s data as an example, since 10,000 transactions per second is our rough estimate for the average, we’d probably need to be able to handle around 100,000 transactions per second to really kill it (one order of magnitude higher than the average, similar to Visa). That’s a lot. More precisely, that’s about 10,000 times faster than Bitcoin—a whopping difference of four orders of magnitude.

To me, this says that our methods of finding consensus on a blockchain are simply not fast or powerful enough to actually use crypto as a viable currency. We need innovations in infrastructure, hardware, and consensus algorithms in order to even hope to reach this threshold.

Bitcoin Is Not the Future of Crypto

Derek Sorensen believes Bitcoin is definitely not the future of crypto. | Source: Shutterstock

That is to say that, barring some major changes and improvements, Bitcoin is almost certainly not the future of crypto.

Technologies like the Lightning Network attempt to solve the scalability problem, but do so awkwardly and ineffectively. Opening channels to transact off-chain ties up money in extremely inconvenient ways. In practice it incentivizes users to open a single channel with a centralized liquidity provider on the blockchain, rather than opening many channels. This effectively creates unregulated, centralized banks, and in my view goes against the core principles of blockchain technology. Even worse, because transactions are done off-chain and channel data can’t be deterministically rebuilt, if a Lightning node crashes, both parties can easily lose funds. It may genuinely be one of the worst ideas in cryptocurrency.

Notwithstanding, the blockchains of the future may not be so far off. New research in math shows promising results in the mathematical foundations of consensus that could produce blockchains with 50,000 transactions per second or more without compromising safety or decentralization. Every day, a new paper comes out or a crypto startup launches a new product.

There are plenty of bright minds working on securing the crypto dream. I guess in twenty years if you’re paying for your groceries with crypto you’ll know that we succeeded.

About the Author: Derek Sorensen, Pyrofex Research Mathematician, has an MSc in Mathematics and Computer Science from the University of Oxford and is set to start his PhD this fall at the University of Cambridge, where he will study logic and topology. His work at Pyrofex is in formal verification, which includes research on the theory of consensus and setting up mathematical frameworks to prove theorems about code.

[ad_2]

Source link